Turn Your Curiosity Into Discovery

Airlines

Facts

Celebrity

Facts

Characters

Facts

Pokemon

Facts

Culture & The Arts

Facts

Games and Toys

Facts

Mass Media

Facts

Performing Arts

Facts

Visual Arts

Facts

Earth & Life Science

Facts

Biology

Facts

Earth Sciences

Facts

Nature

Facts

Physical Sciences

Facts

Events

Facts

Fitness & Wellbeing

Facts

Dentistry

Facts

Exercise

Facts

Health Science

Facts

Hygiene

Facts

Medicine

Facts

Nutrition

Facts

Psychology

Facts

Public Health

Facts

General

History

Facts

Culture

Facts

Historical Events

Facts

People

Facts

Religion

Facts

Human Activities

Facts

Human Activities

Facts

Impact of Human Activity

Facts

Lifestyle

Facts

Entertainment

Facts

Food

Facts

Health

Facts

Sports

Facts

Mathematics & Logic

Facts

Fields of Mathematics

Facts

Mathematical Sciences

Facts

Mathematics

Facts

Movie

Facts

Nature

Facts

Animals

Facts

Human Body

Facts

Plants

Facts

Universe

Facts

Philosophy & Thinking

Facts

Philosophy

Facts

Thinking Skills

Facts

Reviews

Facts

Science

Facts

Biology

Facts

Chemistry

Facts

Geography

Facts

Physics

Facts

Technology

Facts

Society & Social Sciences

Facts

Social Sciences

Facts

Society

Facts

Tech & Sciences

Facts

Agriculture

Facts

Computing

Facts

Electronics

Facts

Engineering

Facts

Transport

Facts

World

Facts

Cities

Facts

Countries

Facts

Landmarks

Facts

US States

Facts

All Categories

Everything Else

Facts

Forum

Gallery

Quotes

Airlines

Facts

Celebrity

Facts

Characters

Facts

Pokemon

Facts

Culture & The Arts

Facts

Games and Toys

Facts

Mass Media

Facts

Performing Arts

Facts

Visual Arts

Facts

Earth & Life Science

Facts

Biology

Facts

Earth Sciences

Facts

Nature

Facts

Physical Sciences

Facts

Events

Facts

Fitness & Wellbeing

Facts

Dentistry

Facts

Exercise

Facts

Health Science

Facts

Hygiene

Facts

Medicine

Facts

Nutrition

Facts

Psychology

Facts

Public Health

Facts

General

History

Facts

Culture

Facts

Historical Events

Facts

People

Facts

Religion

Facts

Human Activities

Facts

Human Activities

Facts

Impact of Human Activity

Facts

Lifestyle

Facts

Entertainment

Facts

Food

Facts

Health

Facts

Sports

Facts

Mathematics & Logic

Facts

Fields of Mathematics

Facts

Mathematical Sciences

Facts

Mathematics

Facts

Movie

Facts

Nature

Facts

Animals

Facts

Human Body

Facts

Plants

Facts

Universe

Facts

Philosophy & Thinking

Facts

Philosophy

Facts

Thinking Skills

Facts

Reviews

Facts

Science

Facts

Biology

Facts

Chemistry

Facts

Geography

Facts

Physics

Facts

Technology

Facts

Society & Social Sciences

Facts

Social Sciences

Facts

Society

Facts

Tech & Sciences

Facts

Agriculture

Facts

Computing

Facts

Electronics

Facts

Engineering

Facts

Transport

Facts

World

Facts

Cities

Facts

Countries

Facts

Landmarks

Facts

US States

Facts

All Categories

Everything Else

Facts

Forum

Gallery

Quotes

Latest Facts

Sports

31 Jan 2026

30 Facts About LSU Basketball

Sports

31 Jan 2026

25 Facts About KC Boutiette

Home

General

Facts

General Facts

Education

Facts

General

31 Jan 2026

25 Facts About Jacks

General

12 Jan 2026

25 Facts About Labels

General

29 Dec 2025

25 Facts About Change

General

29 Dec 2025

25 Facts About Threats

General

28 Dec 2025

25 Facts About Stuff

General

28 Dec 2025

25 Facts About Months

General

28 Dec 2025

25 Facts About Oil

General

28 Dec 2025

25 Facts About Humans

General

28 Dec 2025

25 Facts About Majors

General

28 Dec 2025

25 Facts About Bases

General

27 Dec 2025

25 Facts About Seek

General

24 Nov 2025

20 Facts About Central Concept

General

26 Oct 2025

25 Facts About Class Education

General

26 Oct 2025

30 Facts About PDT Pacific Daylight Time

General

17 Oct 2025

35 Facts About Score

General

03 Oct 2025

20 Facts About AIRES

General

01 Oct 2025

30 Facts About Basement Flooding Prevention And Solutions

General

28 Aug 2025

15 Facts About Gate

General

27 Aug 2025

24 Facts About BMNR

General

19 Aug 2025

Home Equity Loans vs HELOCs Which Is Better for Your Kitchen Renovation

General

15 Aug 2025

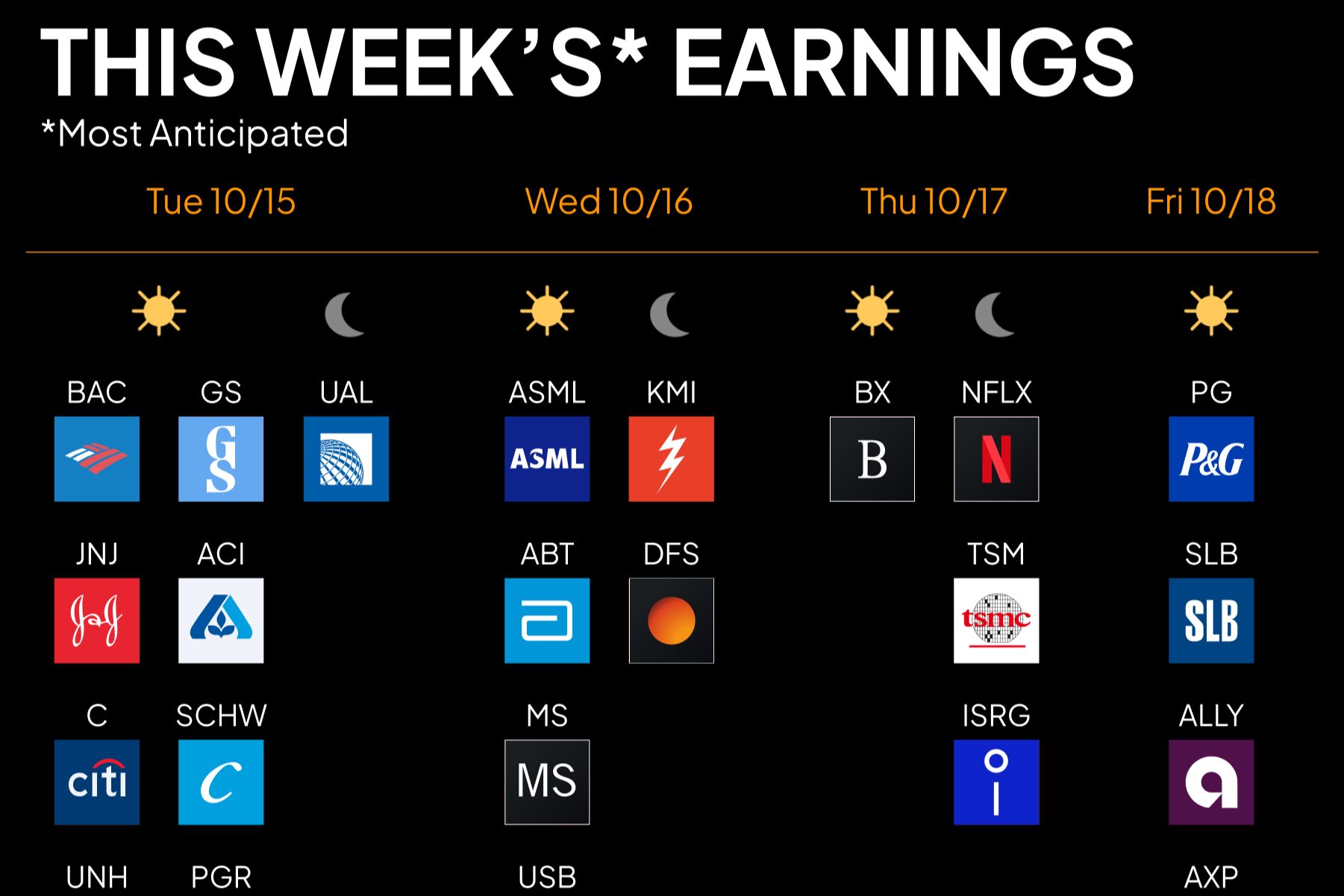

20 Facts About Earnings Calendar

General

15 Aug 2025

20 Facts About Highest 2 Lowest

General

15 Aug 2025

20 Facts About Squad

General

06 Aug 2025

30 Facts About Creative Commons

General

22 Jul 2025

25 Facts About Crowds On Demand

General

20 Jul 2025

20 Facts About Chipotle

General

13 Jul 2025

50 Facts About SOUN Stock

General

13 Jul 2025

50 Facts About SoFi Stock

General

11 Jul 2025

25 Facts About Roman Candles

General

10 Jul 2025

30 Facts About TCU Texas Christian University

General

10 Jul 2025

25 Facts About National And Digital IDs

General

04 Jul 2025

13 Facts About Bill

General

26 Jun 2025

25 Facts About The Hull Of A Boat

General

25 Jun 2025

10 Facts About The Artist Nada

General

21 Jun 2025

14 Facts About OSCR Stock Oscar Health

General

21 Jun 2025

15 Facts About COIN Stock Coinbase

General

19 Jun 2025

10 Surprising Facts About The Word On

General

19 Jun 2025

20 Facts About The Weizmann Institute

General

17 Jun 2025

25 Facts About Gas Prices And Trends

General

16 Jun 2025

20 Facts About The Mega Millions Jackpot

General

16 Jun 2025

25 Facts About The Concept And History Of Spying

General

14 Jun 2025

8 Facts About Visa Bulletin

General

13 Jun 2025

8 Facts About Alabama Power Outage

General

13 Jun 2025

8 Facts About Lotto America

General

11 Jun 2025

12 Facts About XRP News

General

11 Jun 2025

8 Facts About Alabama Power

General

10 Jun 2025

20 Facts About Circle Stock

General

10 Jun 2025

20 Facts About Broadcom Stock

General

10 Jun 2025

20 Facts About Lulu Stock

General

09 Jun 2025

15 Facts About Avgo

Posts navigation

1

2

…

38

Next

Trending Facts

General

16 Jan 2020

300 Crazy Fun Facts To Start Your Day

General

06 Feb 2020

100 Interesting Facts That Will Boggle Your Mind

General

31 Jan 2020

300 Random Facts No One Knows What To Do With

General

07 Feb 2020

100 Nutrition Facts To An Easier And Healthier Lifestyle

General

04 Feb 2020

100 Amazing Facts That Will Blow Your Mind

General

31 Jan 2020

300 WTF Facts That Will Make You Question Everything

General

17 Jan 2020

300 Weird Facts To Confuse And Amaze You

General

07 Feb 2020

100 Did You Know Facts Most People Have Never Heard About

16 Jan 2020

06 Feb 2020

31 Jan 2020

07 Feb 2020

04 Feb 2020

31 Jan 2020

17 Jan 2020

07 Feb 2020